The American Birding Association has a relatively new Executive Director (Nikki Belmonte) and changes are coming. One proposal is modernizing the Bylaws, which govern the structure and operation of the ABA. Most of the proposed changes are sensible, but, as described below, one is troubling.

In the October 2022 issue of Birding, there is a note from Ms. Belmonte stating that the Board of Directors has proposed Bylaw changes and that additional information can be found on the website. As to the purposes of the proposals, she wrote: “The changes instill means for the ABA to operate with layers of oversight and guidance, as well as enable the organization to utilize electronic means to conduct official business.”

The deadline to vote is November 10, 2022, but If history is an indicator, 99% of ABA members will not vote. Indeed, proxy votes seem to pass with under 150 votes. In 2020, for example, candidates for the Board were approved with approximately 130 votes, out of more than 10,000 members.

As far as I can tell (and I may have missed something), so far the only way to locate any information about the proposed Bylaw changes is to manually enter the website identified in Birding into a browser. There are no links in emails to members or on the ABA website. This form of communication is not designed to make the proposals easily accessible to ABA members, but perhaps additional communications are coming. (10/28/22 Update: The ABA did send several email notifications to members.)

A look at the proposed changes seems warranted, as the Bylaws are effectively the ABA Charter. The ABA provided a helpful “Index of Proposed Changes to Bylaws” and it describes most of the proposed changes at a high level. They largely appear designed to update operations and particularly communications to reflect current electronic communications practices. Such changes reflect the realities of the 2020s and make abundant sense.

When lawyers review changes to documents, they typically run a redline, which is a single document that highlights all modifications (both additions and deletions). A redline of the existing and proposed Bylaws is here. (I created this, as it was not provided on the ABA website.) Although it looks messy, a redline is a good way to track changes to a document. Some changes, particularly deletions, are otherwise difficult to identify.

As set forth in previous posts, the ABA has long been in financial trouble, in debt and routinely running annual operating deficits. The ABA’s accountants question whether it can continue as a “going concern.”

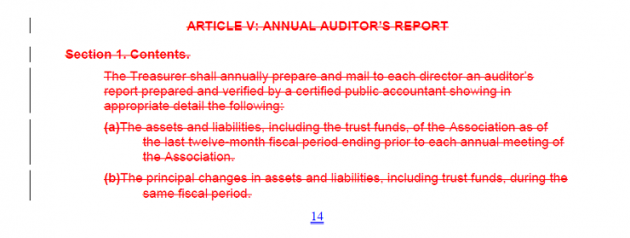

Thus, it is surprising that one of the proposed changes is the wholesale elimination of the Annual Auditor’s Report (redline excerpt below). The existing Bylaws (Art. V) require a report from a certificated public accountant showing: assets and liabilities, principal changes in assets and liabilities, revenue, and expenses. The report must be made available to members and an abstract entered into the minutes of the next annual meeting. The 2020 Report is here.

For an organization that struggles to stay solvent, it seems sensible to have an auditing requirement. However, the proposed changes eliminate this requirement completely.

Moreover, this change is not included in the Index of Proposed Changes to Bylaws. Thus, there is no explanation for why the Board thought this change would be appropriate. One hopes this was an oversight.

Without an explanation, this appears to be a big step backwards in terms of accountability and transparency.

It seems to me that the ABA should not only keep the auditing provisions, it should add a new requirement that the key information be included in an annual report that is sent to membership. This is the practice of many non-profits, from the very large (e.g., National Audubon Society) to the medium-sized (e.g., Portland Audubon) to the small (e.g., Birdability). If a new non-profit with a fraction of the ABA’s resources (Birdability) can prepare and distribute an annual report, then the ABA can too.

An annual report requirement would also be consistent with the BBB Standard for Charity Accountability. The BBB recommendation is:

Annual Report – Have an annual report available to all, on request, that includes: a) the organization’s mission statement, b) a summary of the past year’s program service accomplishments, c) a roster of the officers and members of the board of directors, and d) financial information that includes (i) total income in the past fiscal year, (ii) expenses in the same program, fund raising and administrative categories as in the financial statements, and (iii) ending net assets.

The ABA appears to need more financial discipline, oversight, and accountability, not less. Since these changes are nominally subject to a vote of ABA members, they should also be given more publicity and all changes should have been included in the summary.

Staring at the proxy ballot via the ABA site, it only allows a member to vote yes for the bylaw changes. No is not an option. Rather than being able to vote for Directors, the only option is to delineate which Directors one is voting no for.

Clearly the bylaw changes will eliminate one of the HQ locations, the Delaware City one being the likely target.

I receive emails about the upcoming Bird of the Year reveal party and ABA travel on a regular basis. Not one email about this. I am already awaiting the annual end-of-the-year fundraising/donation appeals.

I believe the only way to vote “no” is not to vote “yes.” Something passes if it gets a majority of the votes of those present or having given a proxy. Thus, a blank vote for the proposed amendments is a “no” vote. At least that’s my reading of the Bylaws.

Email about proxy vote sent to members today.